This is a sponsored post but all thoughts are my own.

More than 1 million children were victims of identity theft or fraud last year, according to the Federal Trade Commission. ONE MILLION last year alone and two-thirds of those victims were 7 years old or younger. I was shocked to learn these statistics, mostly because I hadn’t really heard much about child identity theft. Why is so little said about this important topic if it’s so prevalent? I wanted to share some information today in hopes that it would help shine a light on this digital safety concern.

How does child identity theft happen?

Every day, more and more social security numbers for children are sold on the dark web. As parents we try to safeguard our children’s social security numbers (like we do our own) but they still can end up in the wrong hands when we provide them to places that request them like schools, sports, and camps. Personally, I always ask if it’s necessary to write down my child’s social security number in the space provided on forms and, more often than not, I’m told not to worry about it. I wish those places would just remove that request from their forms if it’s not needed!

Why is child identity theft such a growing problem?

Child identity theft is one of the fastest growing crimes and such an issue because this type of theft can go undetected for years. Parents tend to check their credit often but do not think to do so for their child’s credit because they know their child hasn’t taken out loans, gotten credit cards, or done anything else that would impact their credit. It’s not until the child becomes a young adult and attempts to apply for a car loan or tries to open a credit card and gets denied that they even look at their credit. If someone else used their identity they have to deal with unravelling years and years of defaulted accounts. On top of that, tracking down the person who used their social security number can be an impossible task all those years later.

What can parents do to protect their children?

One of the best things that parents can do for their child’s future financial well-being is monitor their credit now, while their child is young. Parents can get copies of their child’s credit report but that will only detect some types of identity fraud and doesn’t help avoid the headache-inducing frustration of trying to stop identity theft if it’s discovered. Thankfully, there are services like Identron that do all the work for you.

What is Identron?

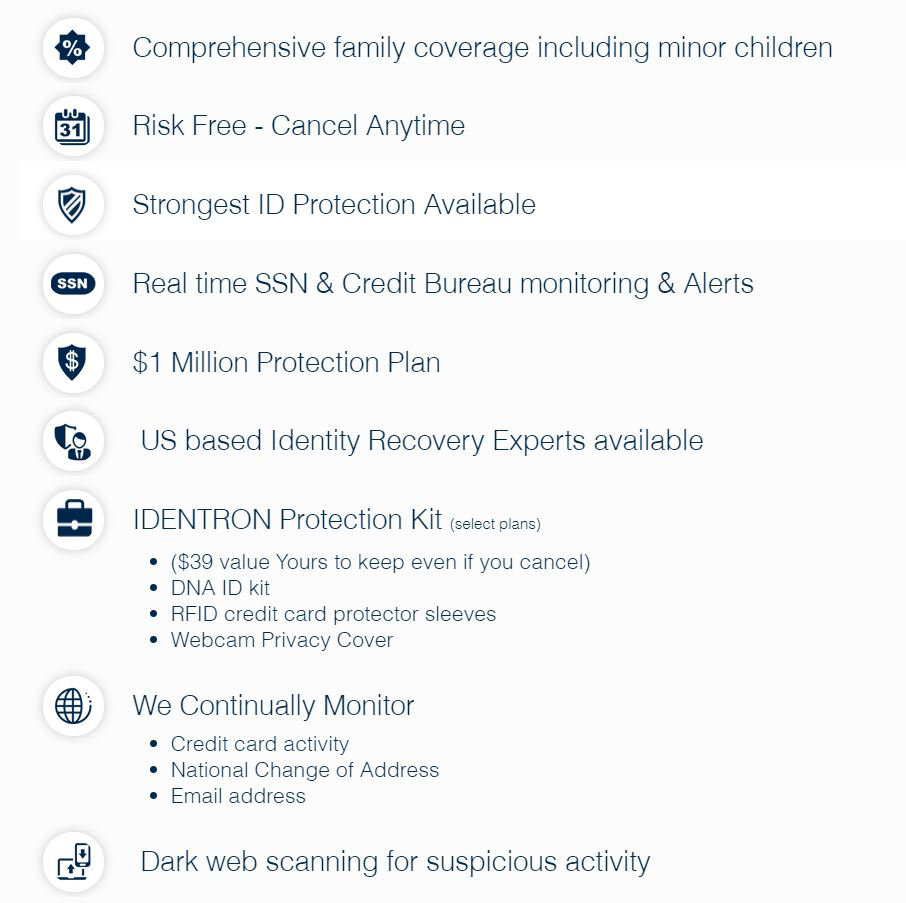

The Identron identity protection plans offered by Identity Protection Planning are hands down the most comprehensive plans, especially when it comes to family coverage, on the market. Identron monitors your family’s personal information in many ways and also makes sure that none of your personal information is being sold on the dark web. All the plans are bottom line a 1-million-dollar insurance policy and have US based identity recovery experts available to help in the event they are needed. You can see all the plans here but the benefits Identron plans offer include:

As parents it is our job to protect our kids and, nowadays, this includes safeguarding their identities. The Identron plans give parents peace-of-mind knowing that they are protecting their child’s identity from theives who seek to use the child’s personal information for their own benefit.

")